China's "economic capillaries" are becoming more cautious, digital, female and solo

A six-year survey conducted by PKU and Ant Research offers a clear picture of the transformation that China's micro and small business operators are going through.

China's micro and small enterprises, or MSEs 小微企业, refer to the smallest end of the country's business sector. They are small employers and everyday businesses that keep local economies running, from neighborhood restaurants and retailers to small manufacturers, service providers, and start-ups.

Small as they are, MSEs form the everyday fabric of the economy. In Chinese policy discourse, they are described as the "capillaries" of the economy: small, widely distributed, and vital to keeping economic activity flowing. They are also an important force for innovation, job creation, and improving people's livelihoods.

As of September 2025, China had 63.487 million small and medium-sized enterprises, of which 98.1 percent were MSEs, according to a report released by the China Internet Network Information Center.

Today's newsletter features excerpts and analysis from a survey on China's MSEs. The Online Survey of Micro-and-small Enterprises, or OSOME, was jointly launched in the third quarter of 2020 by Peking University and the Ant Research. The survey has continued since then and has accumulated nearly 250,000 samples, offering a clear picture of the transformation that China's micro and small business operators are going through.

On April 28 this year, the Guanghua School of Management at Peking University released a report titled "Empirical Findings Based on a Survey of China's Micro and Small Business Operators基于中国小微经营者调查的实证发现" (hereafter "the report"). Your host read through the full report, selected several interesting sections, and added some notes.

For anyone interested, the full Chinese report has been uploaded to Google Drive. You can download it here.

I. Cautious expectations: why market optimism has not reached small businesses

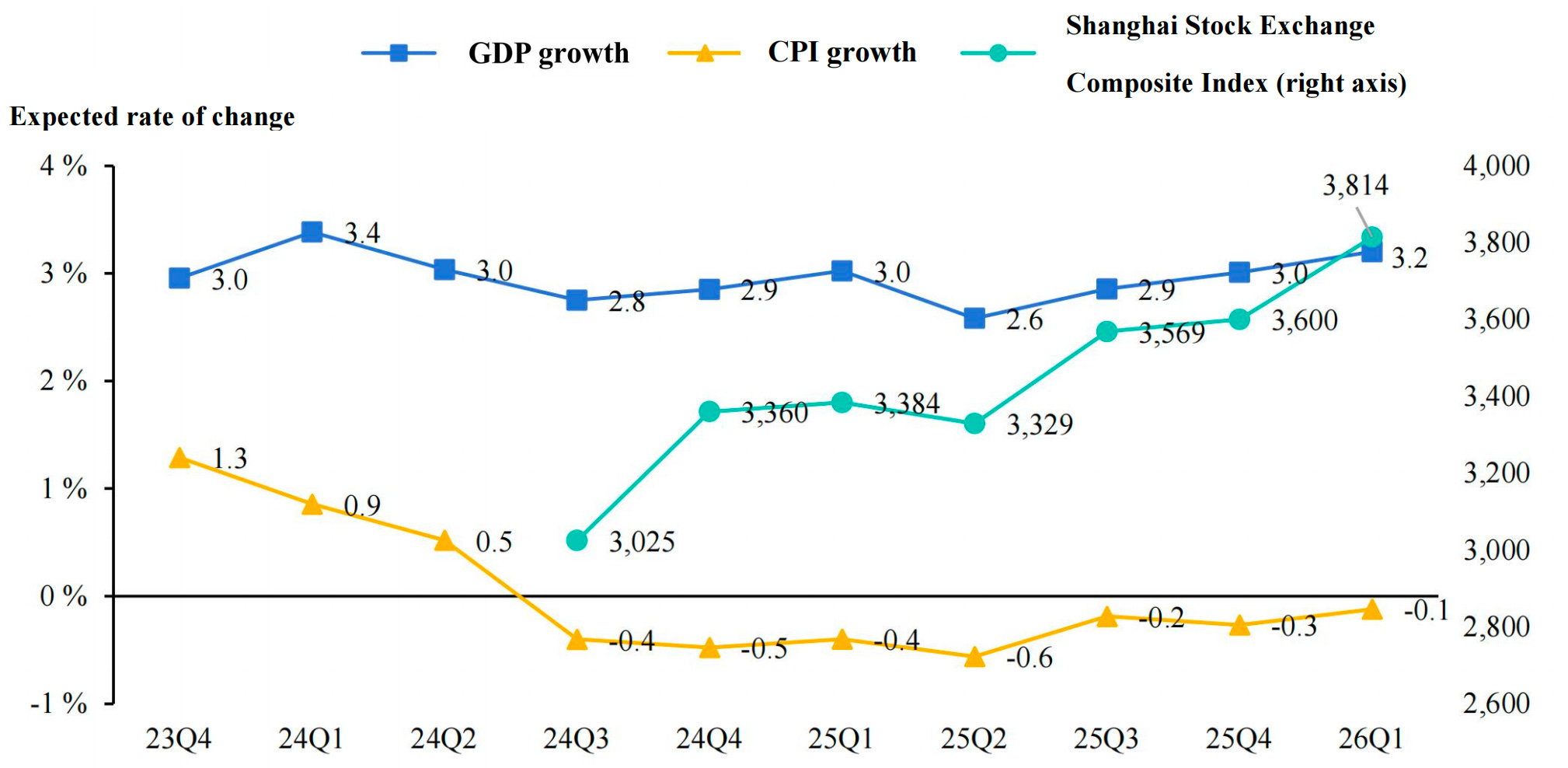

Overall, micro and small business operators remain cautious about the macroeconomy, especially when it comes to expectations for economic growth. Their expectations for GDP growth in the following year have consistently fluctuated between 2.6 percent and 3.4 percent (Figure 4), remaining well below the official target of "around 5 percent."

Moreover, although the economic stimulus package introduced in September 2024 and the positive stock market performance since 2025 helped lift expectations for the equity market, including the Shanghai Composite Index (Figure 4), this optimism did not effectively spill over into other macroeconomic indicators. Nor did it provide a substantial boost to business operators' expectations for their own operations.

This suggests that the recovery signals seen in the capital market have not fully translated into broad-based confidence among micro and small business operators in the real economy. The improvement in expectations remains largely confined to the financial sphere and has yet to reach the micro-level "capillaries" of the real economy. In addition, 30 to 40 percent of micro and small business respondents chose "uncertain" when answering questions about expectations. This highlights a significant lack of confidence and a strong sense of uncertainty at the micro level. The foundation for improving expectations still needs to be consolidated.

Note: This phenomenon shows that the expectations of MSEs are shaped more by the economy as they experience it than by macroeconomic narratives. Although policy stimulus and a stronger stock market have sent positive signals, improvements in the capital market have not automatically translated into confidence in the real economy or in their own business prospects.

For MSEs, what truly shapes expectations are front-line variables such as orders, foot traffic, cash flow, financing costs, payment cycles, and consumer demand. If these operating indicators do not show steady improvement, optimism in financial markets can easily remain at asset prices, without filtering down to the "capillaries" of the real economy.

At the same time, the relatively high share of "uncertain" responses suggests that MSEs are not simply pessimistic. Rather, they lack a clear and stable anchor for expectations. This uncertainty can reinforce a wait-and-see attitude and dampen willingness to invest, hire, and expand. Therefore, the key for future policy is not only to improve macro expectations, but also to strengthen micro and small business operators' real confidence in demand recovery and business improvement through support that is visible, accessible, and sustained.

It is hard to say that the central government has not noticed the importance of "stabilizing expectations". In April 2025, Chinese Premier Li Qiang chaired the State Council’s second special study session of the year. The theme was "strengthening expectation management, and coordinating policy implementation with expectation guidance". Apparently, there is still a long way to go.

II. The share of female entrepreneurs has doubled

From the perspective of gender structure, the share of female micro and small business operators has continued to rise in recent years (Figure 13). This is closely related to the way digital platforms have lowered the capital, time, and space barriers to entrepreneurship, offering women a more flexible and lower-cost path into business.

Compared with traditional offline businesses, online shops depend less on fixed assets and physical premises, allowing women to better balance work and family responsibilities. The credit and evaluation systems within platform ecosystems also help, to some extent, offset the information and credit disadvantages that women often face in traditional financing channels. The research shows that digital platforms have become more inclusive towards female micro and small business operators through risk-control and credit-stratification mechanisms, while women's business activity and retention rates have continued to rise.

Overall, digital platforms have not only expanded the space for women's entrepreneurship, but have also contributed to a structural increase in women's share of the micro and small business economy.

Note: The share of female operators rose sharply from around 17 percent in the third quarter of 2020 to 36 percent today. This reflects the growing inclusiveness and adaptability of digital platforms for women entrepreneurs. At the same time, the inclusiveness of digital finance, including platform transaction records, user reviews, and credit mechanisms, has helped compensate, to some extent, for women's disadvantages in traditional financing and business networks, enabling them to build trust through their operating performance.

In addition, women's experience and communication strengths in sectors such as life services, retail, education, health, beauty, maternity and childcare, and content-driven consumption are highly compatible with the segmented scenarios of the platform economy.

III. Digital transformation and AI adoption

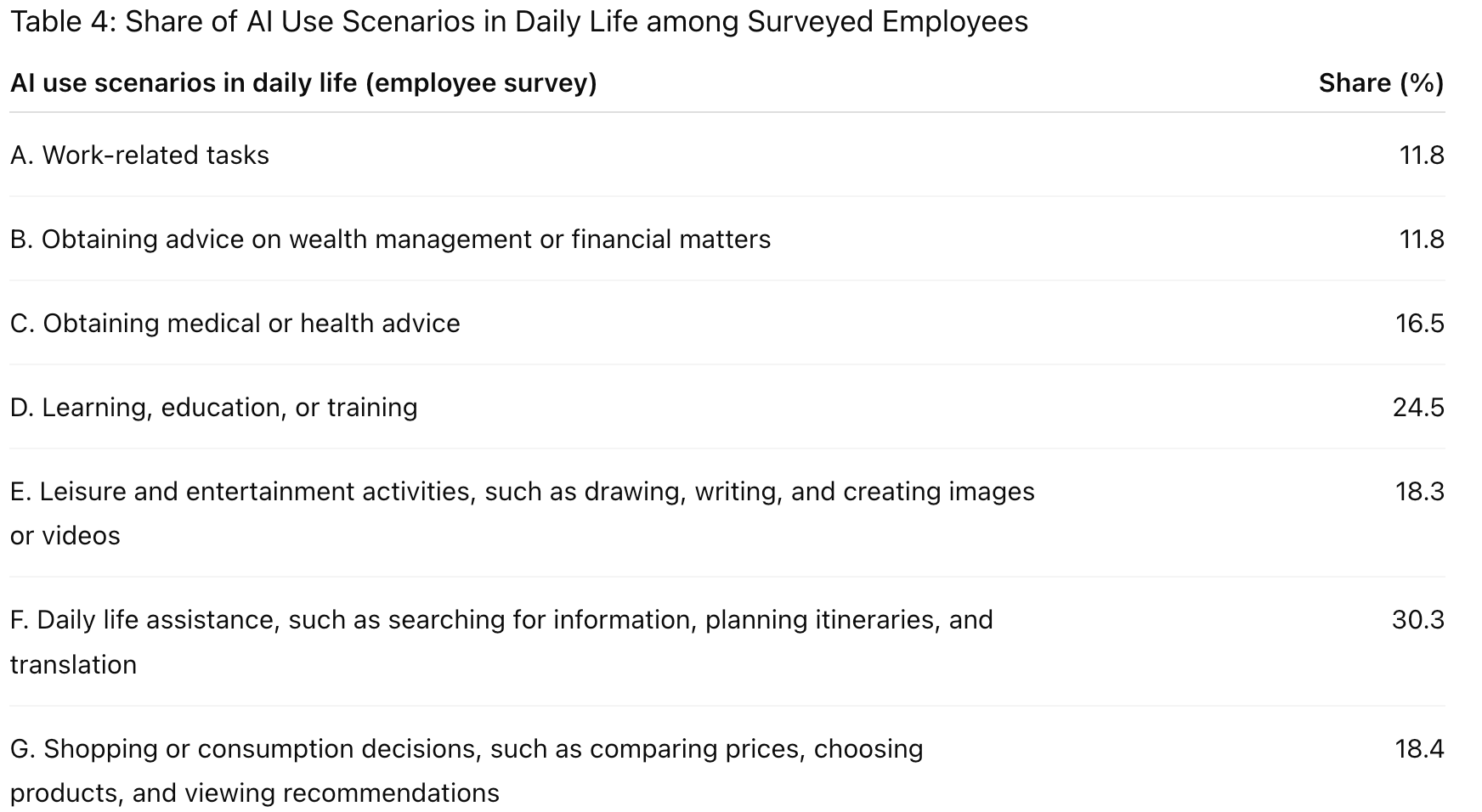

Overall, the use of AI among employees of MSEs is still concentrated in low-threshold, general-purpose, and auxiliary daily-life scenarios. Looking at specific everyday scenarios (Table 4), their use of AI is mainly concentrated in relatively general areas such as information search and learning support.

Daily life assistance, such as searching for information, planning itineraries, and translation, was the most common use case, at 30.3 percent. This was followed by learning, education, or training, at 24.5 percent. A certain share of respondents also used AI for leisure and entertainment, shopping and consumption decisions, and medical or health advice, at 18.3 percent, 18.4 percent, and 16.5 percent, respectively. By contrast, the use of AI for work-related tasks and for wealth management or financial advice remained relatively low.

Note: Overall, the use of AI by MSE owners and employees is still at an early stage of diffusion. AI has already entered the daily lives of this group through low-threshold scenarios such as information search, translation, learning and training, and leisure and entertainment. But it has not yet been fully converted into a tool for business management.

The fact that 24.5 percent of respondents use AI for learning, education, or training is particularly noteworthy. It shows that MSE operators and employees are not rejecting AI. On the contrary, they are actively using it to acquire knowledge, improve skills, and understand new information.

As Cai Fang, former Vice President of the Chinese Academy of Social Sciences, put it, whether AI becomes a blessing or a threat for MSEs depends on whether they can fully make use of its empowering features. This is an exogenous technological change that does not depend on the will of individual firms. If MSEs are to share in the technological dividends, they will need special support. For example, the government could coordinate with large technology companies to take advantage of AI's "zero marginal cost" features and share technology through models, platform APIs, tokens, and other means, helping to close the digital and intelligent divide.

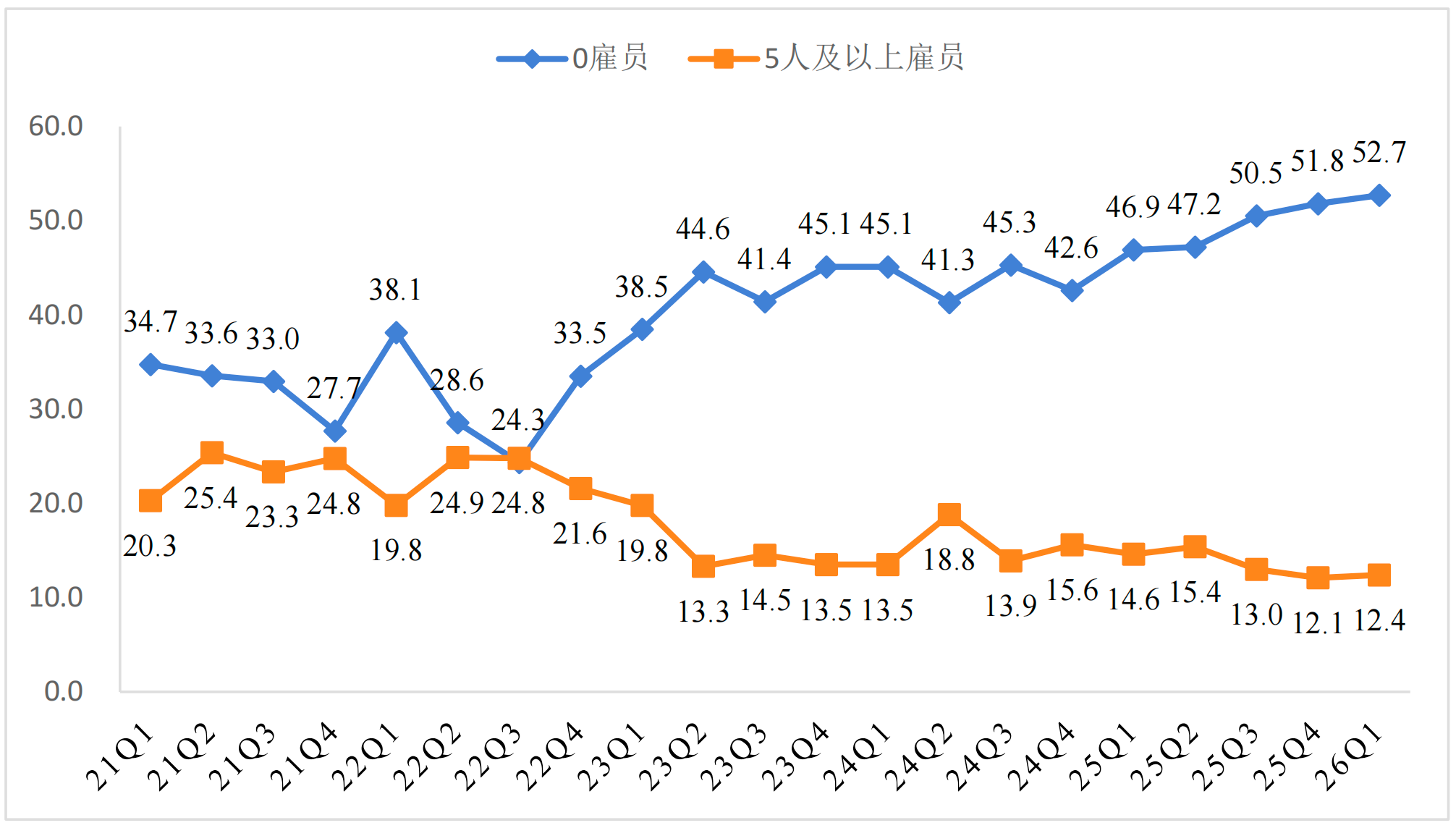

IV. The marked rise of one-person companies (OPCs)

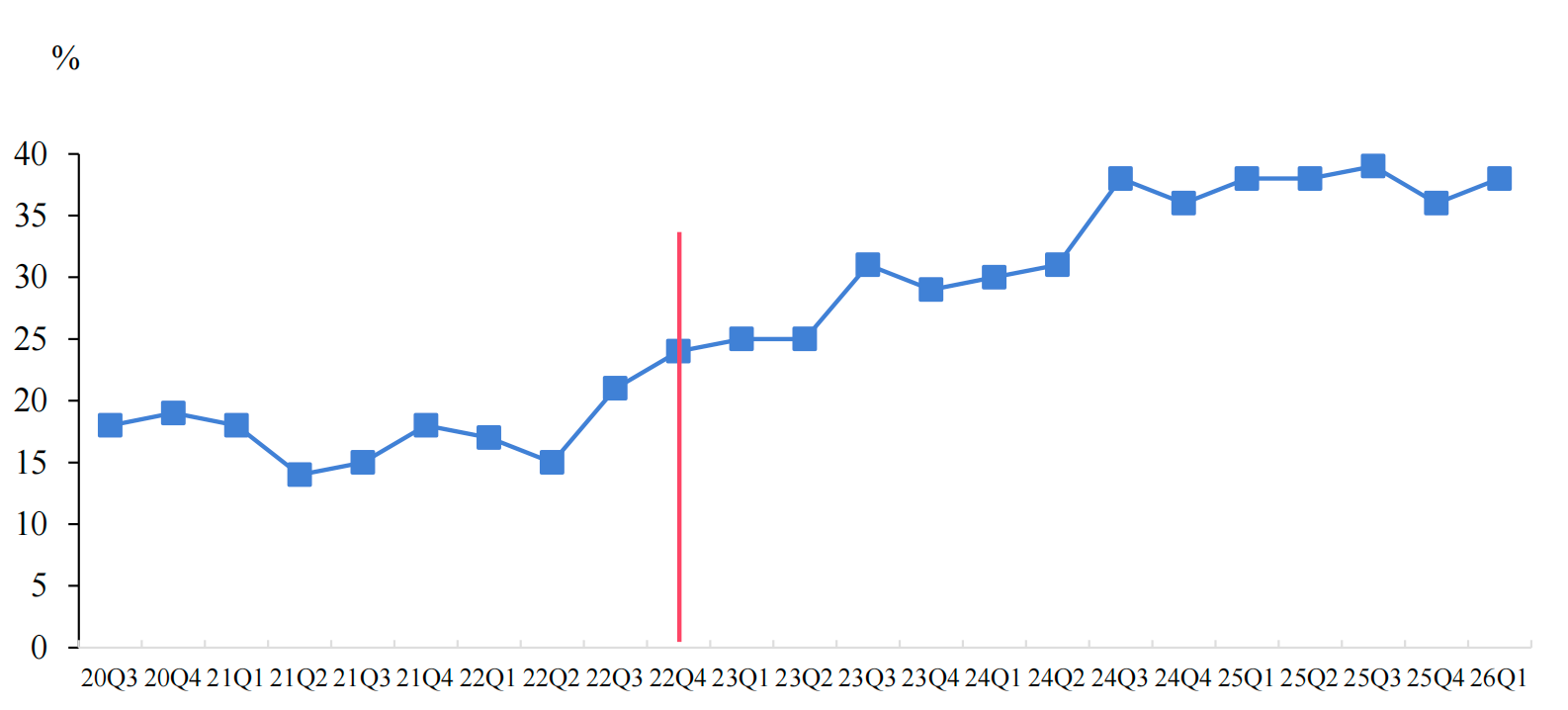

OSOME data show that before the third quarter of 2022, the share of MSEs with zero employees fluctuated at around 30 percent (Figure 18). Starting in the third quarter of 2022, this share began to rise steadily, climbing from 24.3 percent in that quarter to 52.7 percent in the first quarter of 2026, an increase of 28 percentage points.

By contrast, the share of MSEs with five or more employees remained at around 25 percent in 2021 and 2022, but has fallen to 12 percent since the fourth quarter of 2022. The business model of MSEs is showing a clear shift towards lighter assets and lower levels of formal employment.

Note: "One-person companies" (OPCs) have seen rapid growth across China in early 2026. According to a nationwide research report on OPC development released in March, their founders are mainly from the generations born in the 1990s and 2000s.

Micro and small business operators with no employees, in other words, OPCs, have increased from 34.7 percent to 52.7 percent, now accounting for more than half of the total. This trend is closely related to the rise of the gig economy and flexible employment, and is also inseparable from the wider use of AI discussed above.

This shift has lowered the threshold for entrepreneurship and made micro and small business operations more flexible. At the same time, it also means that many MSEs remain small in scale, have limited employment capacity, and face considerable uncertainty. Their ability to absorb employment and achieve stable growth remains to be seen.

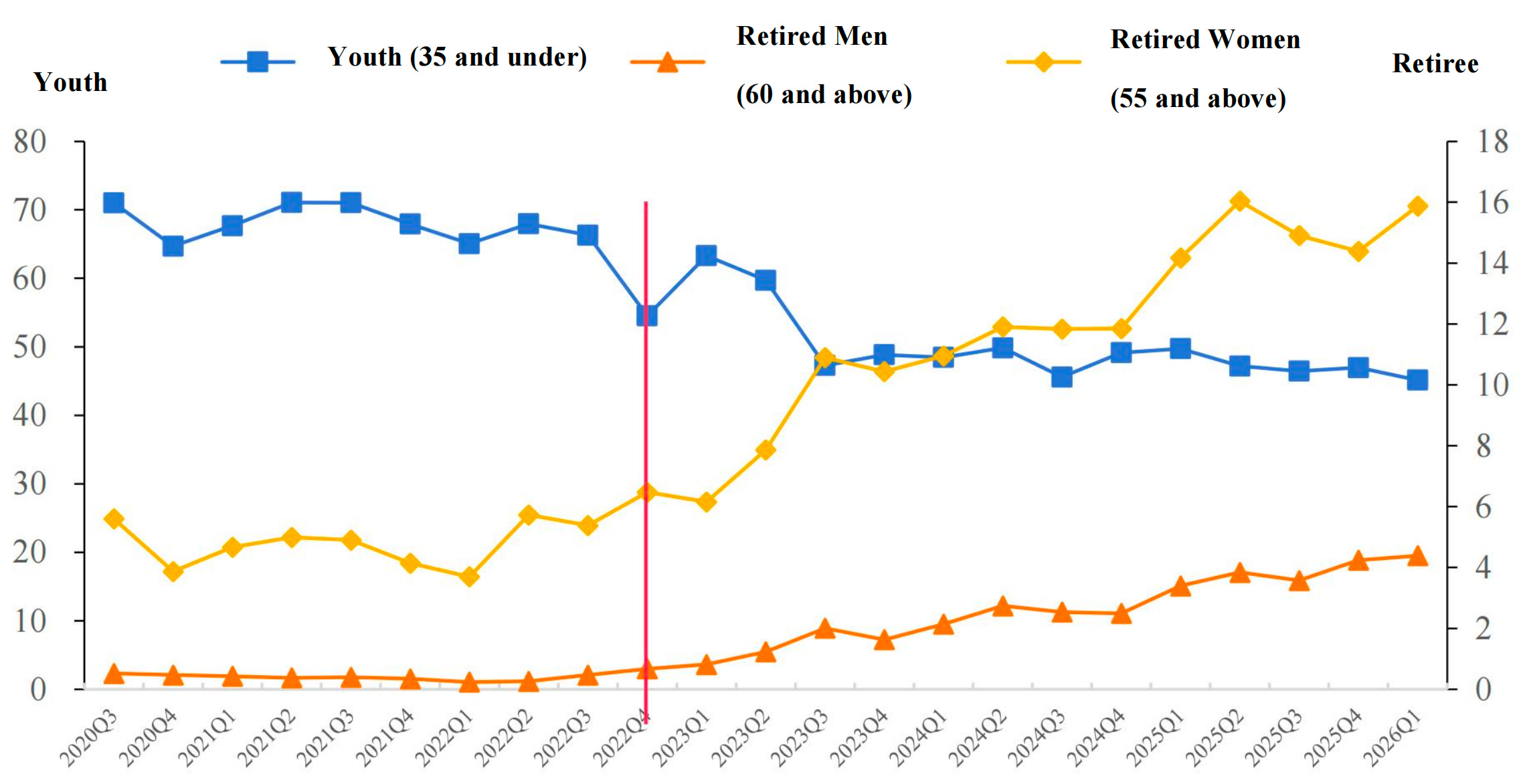

V. Fewer young entrepreneurs, more retirees

From the perspective of age structure, changes in youth participation in entrepreneurship have been particularly noticeable, revealing the strong role of digital platforms in both absorbing and reshaping youth entrepreneurship.

OSOME data show that since 2020, the share of young people among platform-based micro and small business operators has fluctuated significantly. During the pandemic years of 2020 and 2021, the share of young entrepreneurs rose rapidly and reached a peak of around 71.1 percent in the fourth quarter of 2021. As the labor market gradually recovered, this share fell to 45.6 percent in the third quarter of 2024 and has since hovered around 45 percent.

This trend suggests that digital platforms provided young people with an important employment buffer and a channel into entrepreneurship during economic volatility. Young people were able to use digital tools to enter the market quickly and operate flexibly, demonstrating the immediacy and high elasticity of digital entrepreneurship. During the recovery phase, however, some young business operators exited the market, reflecting the temporary and mobile nature of digital entrepreneurship.

Over the past five years, the average age of micro and small entrepreneurs has risen steadily, as has the share of older workers, especially retirees, defined as women aged 55 and above and men aged 60 and above. These shares increased significantly from 5.6 percent and 0.5 percent to around 15.9 percent and 4.4 percent, respectively (Figure 14).

This shows that, as life expectancy rises and average health conditions improve, some older people still retain strong work capacity and a willingness to continue working after retirement. Micro and small business operations provide them with a flexible employment channel. At the same time, some retirees use micro and small business activities to earn extra income and supplement inadequate pensions. Together with the policy environment that encourages the development of the "silver economy", these factors have contributed to the expansion of older micro and small business operators.

Note: During the pandemic, platform entrepreneurship offered young people a rapid-entry employment buffer. As the labor market recovered and platform competition intensified, some young operators exited or shifted towards more stable career paths.

Meanwhile, as healthy life expectancy increased, the need to supplement pensions grew, and digital tools lowered the threshold for business operation, more retirees began to enter the micro and small business sector. Seen this way, the platform-based micro and small economy functions both as a "buffer" for young people facing employment pressure and as an important channel for older people to continue participating in work, increase their income, and maintain social connections.